Hear no evil, speak no evil, own no evil?

Why people who see themselves as moral value investors should own evil companies

"There's some good in this world, Mr Frodo, and it's worth fighting for." So said Samwise Gamgee in the movie version of "The Lord of The Rings: The Two Towers." The scriptwriters, who dreamed up the line, thought it might come across as cheesy but decided to leave it in any way. And thank goodness they did—it's become iconic. But what does good mean? To Frodo and Sam, it meant destroying the ring and getting back their idyllic lives in The Shire. To others, it means avoiding being protested by woke university students. And to many value investors, it means not taking a position in any companies they see as immoral.

The sanctimonious among us won't invest in coal mines or cigarette makers because they think soot and smokes are nasty. They reckon that the companies who make those things are evil. They don't want their dollars going to support those causes. However, their logic is misguided. It's precisely because these investors think those companies are evil that they should invest in them. By doing that they will enjoy better returns, help prevent money from getting into the hands of folks they deem evil, and they can affect change.

First, you should invest in companies you think are evil because it will help prevent the wrong sorts of people from benefitting from that business's cash flows. All companies have an owner. Someone receives the company's dividends whether you like it or not. If you view yourself as good and think you'll do moral things with your money, you should buy evil companies from bad people. That will stop those villains from profiting from those businesses. After all, if you see them as evil, surely you want to prevent them from enjoying those profits?

Imagine it's the 1940s, and a large investment bank is selling, for cheap, a big malevolent company that makes lots of money. All else being equal, would the world be better off if the Nazis or The Red Cross bought it? If the Nazis owned it, they would get regular profits and dividends to help fund death camps and the war machine. If The Red Cross owned it, they would have more money to save lives. If you see yourself as a moral investor and don't buy evil companies, you demonstrate that you're okay with evil people enjoying those profits.

That is the same collective agreement most rich countries' citizens have already made. By taxing booze and tobacco makers, for example, more than other companies, governments show that they want a bigger slice of evil companies' pies. We've all indirectly said, give us a big piece of the ownership of those firms' profits, and we'll use that money for good. Lawmakers justify that extra tax because they use it to fund healthcare and education, both virtuous things. But actually, it's an entity, the state, that wants to own a piece of an evil company to use the profits for what it sees as good. Many people identifying as moral investors have already accepted this logic without realising it.

You should also buy evil companies because competition will force them to act better in society's eyes. By investing in those companies, you're contributing to lowering their cost of capital. A lower cost of capital means companies in that industry can raise money and reinvest more than they otherwise would. That drives up competition, which lowers the prices these evil companies charge. Consumers will have more selection and control over which firms they buy from. And, all else equal, they will go for the company they collectively see as the most ethical.

Whereas, if people collectively sell those evil stocks, their cost of capital will rise. Instead of raising money, companies in that space will divest. Competition will decline, and consumers will have less choice. Shoppers will be stuck with the most ruthless and amoral suppliers. By investing in evil companies, you'll contribute to the moral improvement of the industry. If you don't, you'll let it decline, and the most evil incumbents will become even more dominant.

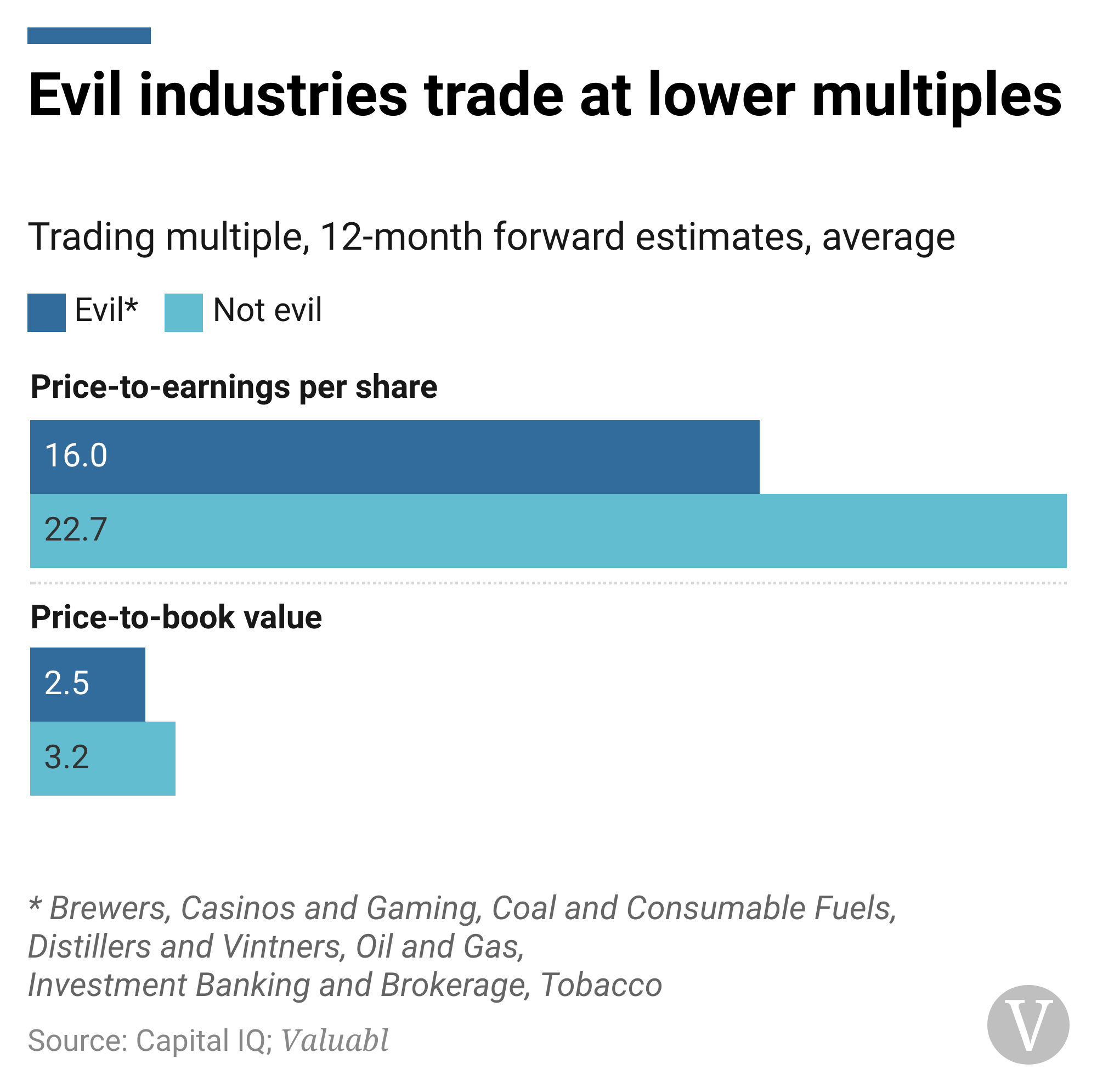

If you see yourself as a moral investor, you should also invest in evil companies because they're cheap—people don't want to own them. According to data from Capital IQ, evil companies tend to trade at lower forward price-to-earnings (PE) and price-to-book (PB) ratios than non-evil ones. The average forward PE ratio for an evil company was 16x, while 23x for non-evil ones. This sample looked at the 20,000 largest companies by market capitalisation.

Of course, whether or not these industries are evil is subjective. However, governments love to vilify and crack down on these sectors, suggesting most see them as the bad guys. Still, other factors could explain why they trade at lower multiples. Perhaps they're systematically riskier? In fact, they're not. Both evil and non-evil companies in the sample have an average beta of one. Maybe they'll grow more slowly? Again, the difference is negligible. Analysts forecast an average two-year revenue growth rate for evil companies of 8.6% and 9.0% for good ones. As a result, the expected returns on evil stocks are better on average than for good ones. It turns out you must be bad to be good. ■